Executive Summary

Despite the addition of two large Utility EIM Members to CAISO (BPA and Tucson Electric), little meaningful new Generation or Load was added to the Seven ISO Grid System during the Second Quarter of 2022. In fact, with the exception of the almost 2.5 GW of Solar and 250 mw of Storage in Ercot, virtually no new Generation was added to US ISO Grid capacity during the most recent quarter.

Second Quarter 2022 PNode Additions

Much discussion is taking place regarding the slow response of regulatory authorities to entities seeking to respond to economic signals regarding absence of new generation or storage capacity, push to make the grid cleaner, and lately legislative initiatives creating new incentives for clean generation and energy storage. One indicator of the efficiency of various regional regulatory bodies have processed requests to build new generation and storage is the speed in which Interconnection Request have been approved. Some projects make their way through the siting and approval process, and some do not. However, one of the most significant phases for any new construction on the Grid is the assignment of a Price Node or PNode by the ISO regulatory authorities. This can indeed occur before any visual satellite evidence of the facility can be seen, or even prior to energy or services being taken from, or provided to the Grid. Still, this is an important designation in the life of the facility (substation or generation) indicating that a unique price for the value of energy is now being published as a result of the ISO SCED (Security Constrained Economic Dispatch) process which produces a Locational Marginal Price (LMP) for the physical location.

Clarity PNode Additions

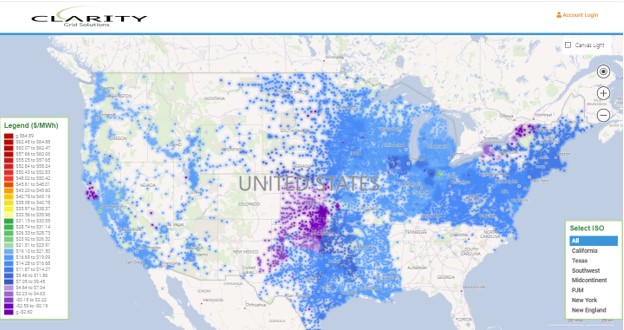

Because the economic and physical structure can best be understood beginning at PNode layer, the current composition of the Load and Generation pricing and location is of great interest to a wide assortment of Grid Stakeholders, renewables developers, marketers and traders, DER developers, and even EV charging infrastructure developers. Therefore, we spend a great deal of effort at Clarity Grid mapping not only the existing set of grid elements but also adding those which appear on a continuing basis through the data feeds of each respective US ISO. Recently a major factor in PNode additions has been the inclusion of an entire Utility’s grid infrastructure as is becomes a member of an existing ISO. CAISO’s introduction of the Energy Imbalance Market (EIM) continues to lead the charge in the additions of entirely new nodal generation and distribution networks, in this quarter adding BPA and its broad network of participating Coops and PUDs, as well as Tucson Electric. This caused CAISO to again add the most new PNodes to the CAISO data series at 1,307 Load Nodes and 408 Generation Nodes, including a large number of existing Hydro Facilities being brought into the fold. Here are the Totals for the 2Q of 2022:

| Load | Gen | |

| NYISO | 0 | 2 |

| NEISO | 17 | 5 |

| MISO | 8 | 0 |

| PJM | 182 | 9 |

| SPP | 38 | 7 |

| ERCOT | 474 | 11 |

| CAISO | 1,307 | 408 |

| Totals | 2,026 | 442 |

New Generation Node Additions by Fuel Type (Storage)

As we track the addition of Generation Pricing Nodes (PNodes) throughout the 7 ISOs it is important to distinguish additions due to new construction as opposed to the addition of new Utility Systems to a particular ISO. Most noteworthy as mentioned this quarter was the Generation sets which were internalized into the CAISO Generation set due chiefly to the addition of BPA’s expansive network and that of Tucson Electric. These entities accounted for 382 of a total addition of 408 Generation PNodes in CAISO. Still while this does represent new Generation Nodes which are eligible now for dispatch into the CAISO EIM (Real Time Market) they do not represent an addition to the generation capacity on the US Grid.

| NYISO | NEISO | PJM | MISO | SPP | ERCOT | CAISO | Totals | |

| Solar | 0.0 | 0.0 | 1,673.7 | 1,165.2 | 0.0 | 1,827.0 | 2,251.7 | 6,917.6 |

| Hydro | 0.0 | 38.6 | 2.2 | 700.0 | 647.0 | 0.0 | 5,814.1 | 7,201.9 |

| Natural Gas | 0.0 | 330.0 | 1,765.3 | 10,137.0 | 2,741.6 | 8,779.9 | 2,157.5 | 25,911.3 |

| BM | 0.0 | 0.0 | 0.0 | 0.0 | 4.8 | 0.0 | 183.4 | 188.2 |

| Battery | 0.0 | 0.0 | 67.8 | 1.2 | 0.0 | 211.0 | 479.0 | 759.0 |

| Wind | 0.0 | 0.0 | 346.2 | 1,617.0 | 6,686.7 | 1,775.6 | 264.4 | 10,689.9 |

| Coal | 0.0 | 0.0 | 0.0 | 0.0 | 325.0 | 0.0 | 0.0 | 325.0 |

| Distillate | 0.0 | 250.0 | 0.0 | 31.0 | 132.0 | 50.0 | 15.0 | 478.0 |

| Generation | 51,711.9 | |||||||

| Storage | 759.0 |

Newly Constructed Generation

If we filter through the New Nodes list and Generation by Fuel type to identify only newly constructed Generation and Storage, we see that (with the exception of Solar and Battery Storage in ERCOT) very little new Generation or Storage capacity came onto the Grid last Quarter as tracked by PNode introductions (see below)

| NYISO | NEISO | PJM | MISO | SPP | ERCOT | CAISO | Totals | |

| Solar | 49.90 | 49.30 | 939.10 | 0.00 | 0.00 | 2,544.30 | 226.00 | 3,808.60 |

| Hydro | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Natural Gas | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 88.00 | 0.00 | 88.00 |

| BM | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Battery | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 246.95 | 142.60 | 389.55 |

| Wind | 0.00 | 0.00 | 118.00 | 0.00 | 0.00 | 0.00 | 0.00 | 118.00 |

| Coal | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Distillate | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Generation | 4,014.60 | |||||||

| Storage | 389.55 |

Noteworthy Examples of New Generation and Load

Taking a look at some specific Generation/Storage Units coming on in the 2Q 2022:

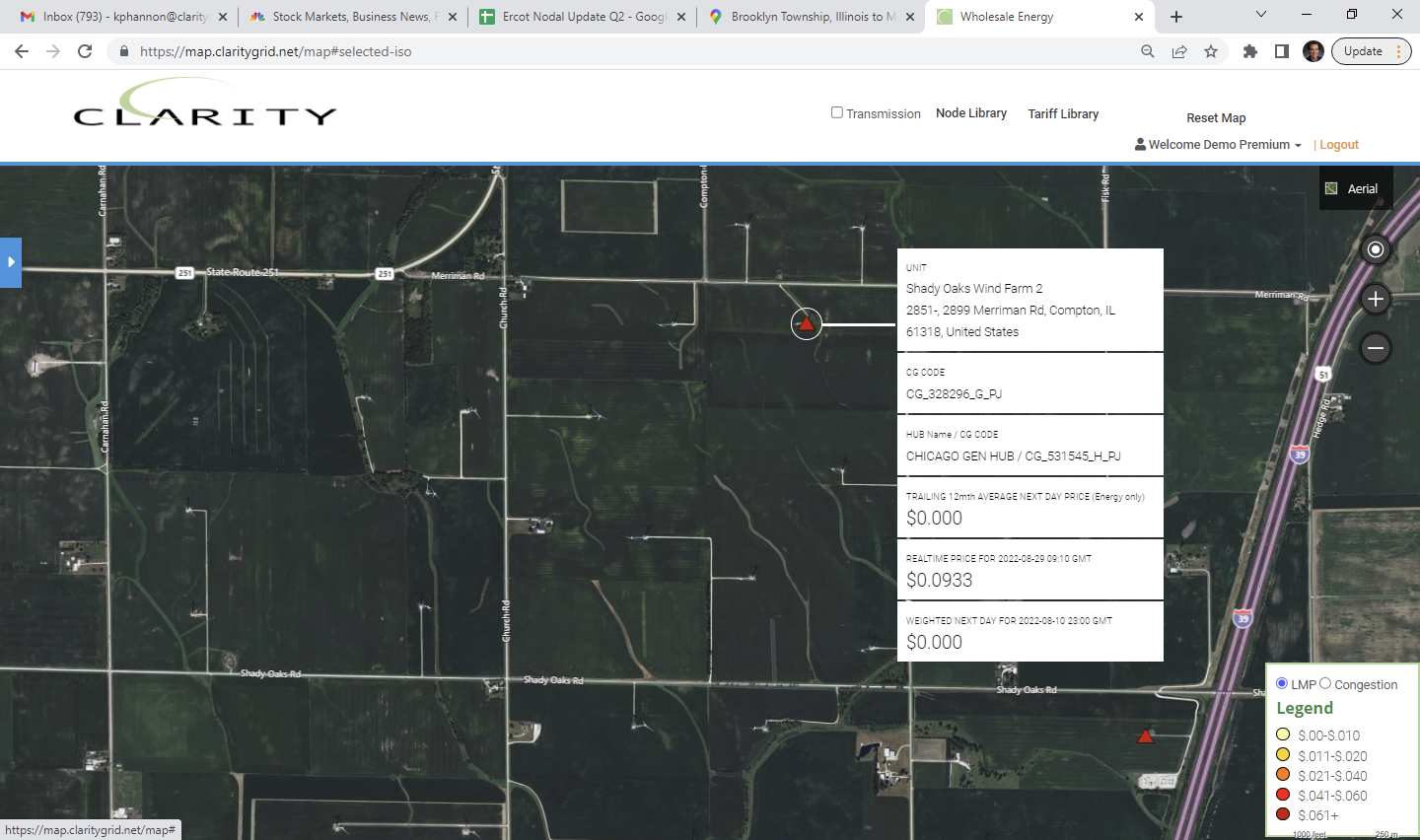

PJM: Shady Oaks Wind Farm 2 Liberty Power 118 mw joining Shady Oaks Wind Farm 1just to the southeast.

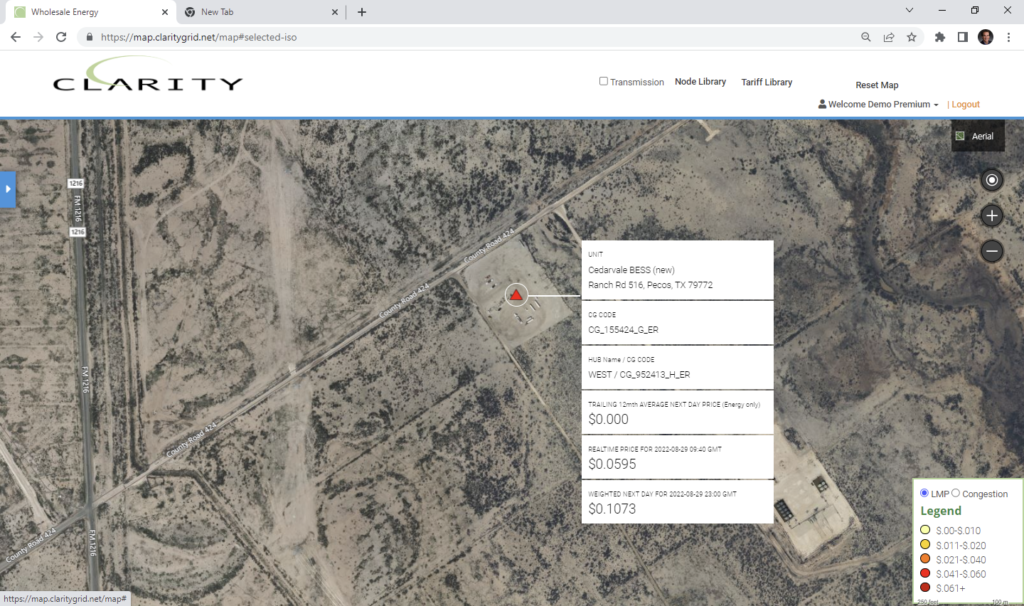

ERCOT Gen: HEN Infrastructure’s 9.9 Cedarvale Battery view of installation under construction

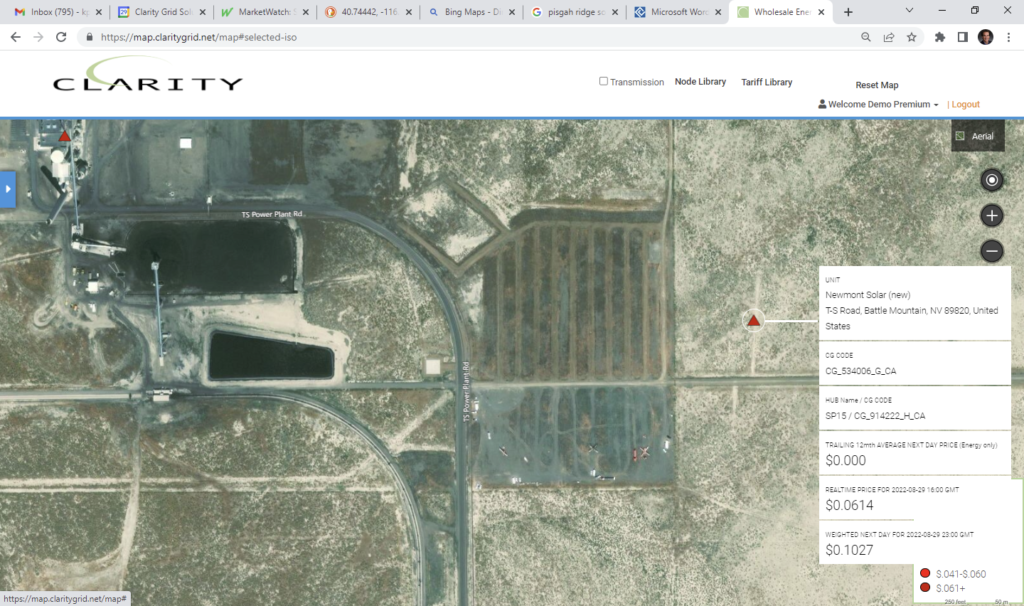

CAISO Gen: Newmont’s new 100 mw Solar Facility under construction adjacent to its Battle Mountain TS Power Plant Facility.

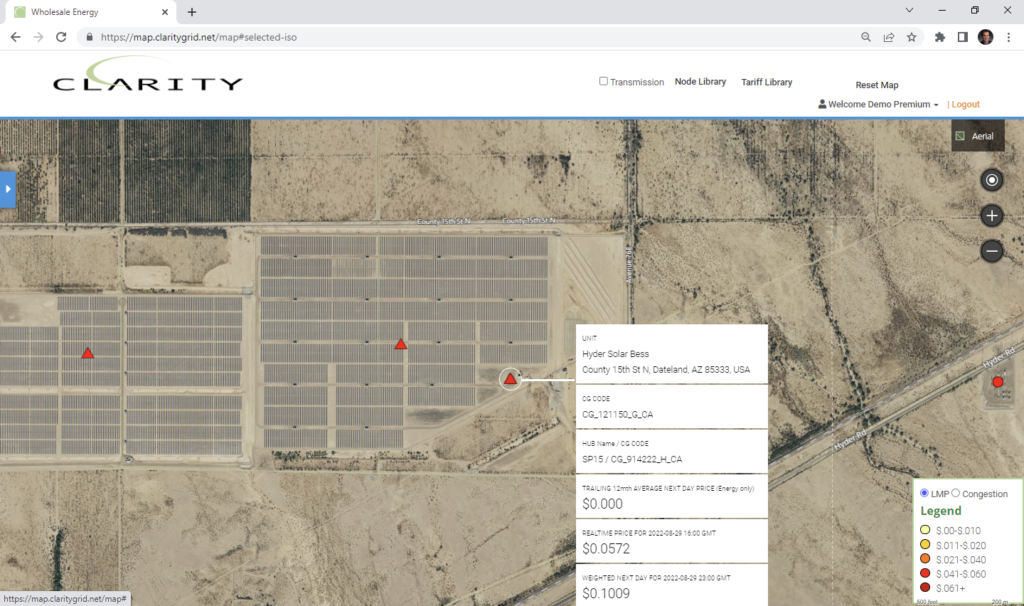

CAISO New Gen: Hyder Solar 22 mw BESS in AZPS Service Territory:

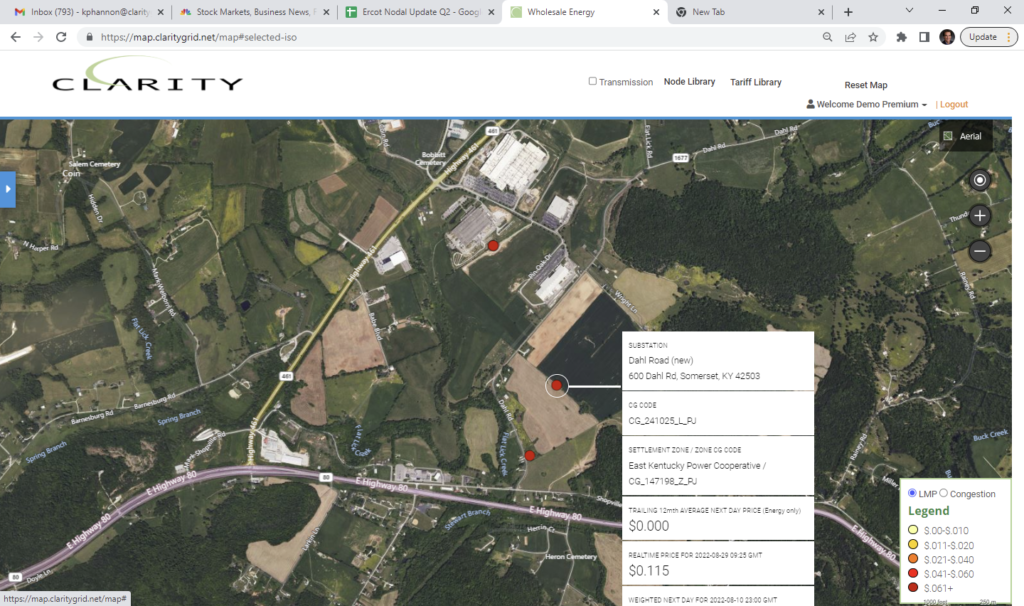

Load PJM: EKPC 69 kv Substation New Dahl Road supports new Toyotetsu America, Inc. (Toyoda Iron Works Co) (TTAI) plant

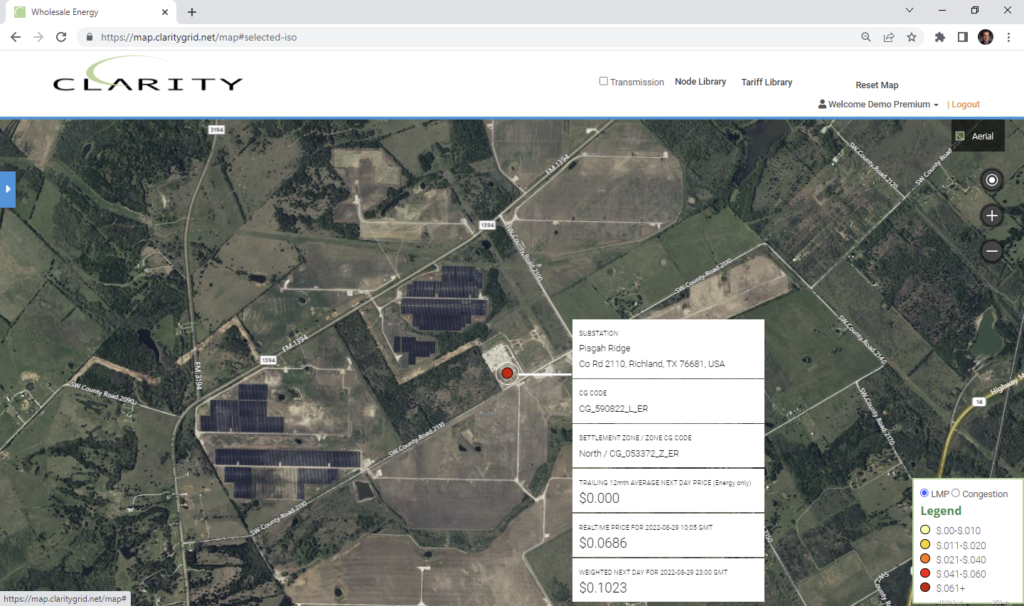

ERCOT Load: Pisgah Ridge 345 kv Substation to support new 250 mw Pisgah Ridge Solar Farm

SPP Load: City of Springfield, MO Utilities new 161 kv Republic substation supports AWS Datacenter under construction to the east.

New Load (Substations):

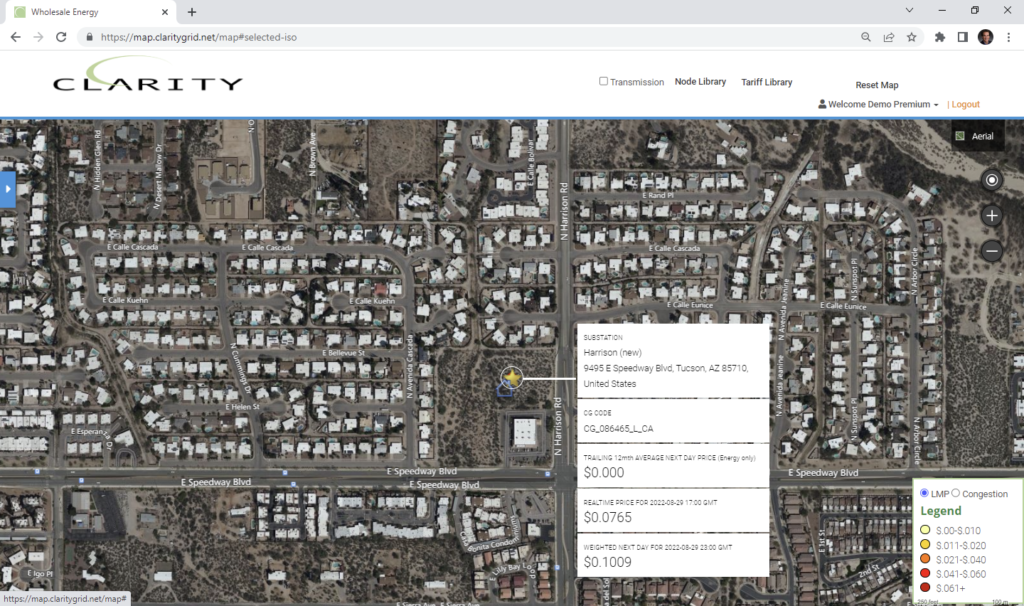

CAISO Load: Tucson Electric new 138 kv Substation under construction:

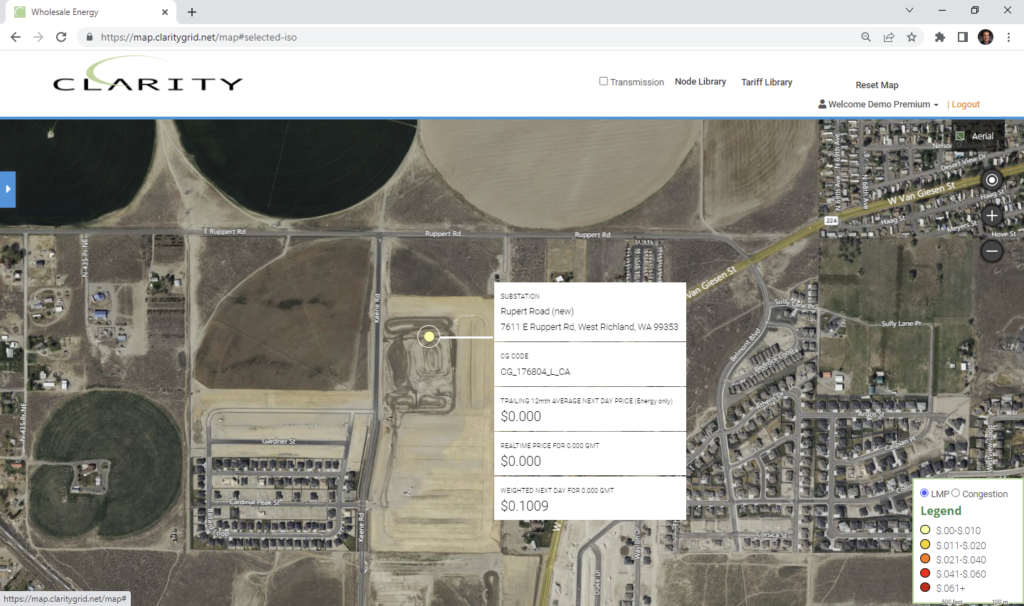

CAISO New Load: Benton Rural Elec Assn 138 kv Ruppert Road substation in BPA territory under construction:

If you are interested in viewing all existing and new load and gen facilities, please inquire about a trial at https://www.claritygrid.net and select “Request a Demo.”